Editorial Note: Forbes might earn a commission on sales made from partner links on this page, but that does not impact our editors' viewpoints or assessments. Simply weeks prior to the brand-new year, mortgage rates are breaking records yet once again. Mortgage rates on the 30-year fixed-rate home loan fell to their lowest point for the 14th time this year, slipping to 2.

The new record may be a little a surprise, as the bond https://www.openlearning.com/u/vernita-qg8bc9/blog/HowDoSecondMortgagesWorkInOntarioCanBeFunForAnyone/ market livened up on Tuesday following whisperings of fiscal relief. Treasury yields, which normally move in tandem with home loan rates, increased slightly, however did not bring house loan rates with them. With home mortgages in high demand and the refinance share of home loan applications up 102% year-over-year, loan provider profits are soaring, according to a current report by the Mortgage Bankers Association.

This, coupled with an aggressive fiscal policy from the Federal Reserve, is what's keeping a lid on rates. "The Federal Reserve's anticipated plans to continue their speed of mortgage-backed securities purchases is likewise likely to keep upward motions in mortgage rates in check," states Matthew Speakman, an economic expert at Zillow.

Home loans to buy a home were up 9% week-over-week, after changing for the Thanksgiving vacation, and were 28% greater than the exact same time in 2015, according to the Mortgage Bankers Association's (MBA) Weekly Home Mortgage Applications Survey for the week ending Nov. 27, 2020. The serious real estate lack has actually pressed the typical purchase loan quantity to $375,000, the greatest level considering that MBA began its survey in 1990.

"The sustained duration of low mortgage rates continues to spark borrower demand, and the mortgage industry is poised for its greatest year in originations since 2003," says Joel Kan, associate vice president of economic and industry forecasting for MBA. "The continuous re-finance wave has actually been useful to house owners seeking to decrease their monthly payments throughout these tough financial times came up with by the pandemic." The typical rate for the benchmark 30-year fixed dropped one basis indicate 2.

Everything about Which Credit Score Is Used For Mortgages

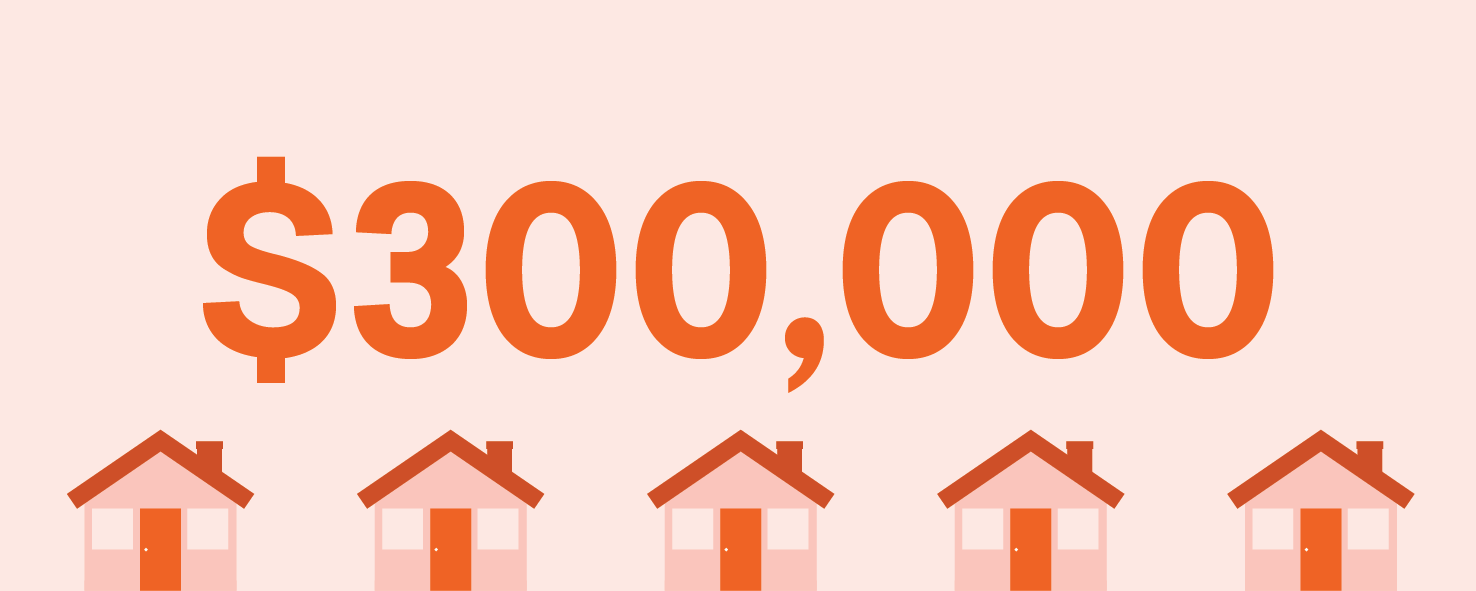

A basis point is one one-hundredth of a percentage point. This time in 2015, the 30-year fixed was 3. 68%. Borrowers with a 30-year fixed-rate mortgage of $300,000 with today's rate of interest of 2. 71% will pay $1,218. 38 per month in principal and interest (taxes and costs not consisted of), the Forbes Consultant home loan calculator programs.

60. That same home mortgage secured a year earlier would cost an additional $57,269. 11 in interest over the life of the loan. The average interest rate on the 15-year fixed home loan dropped two basis points recently to 2. 26%. This time last year, the 15-year fixed-rate mortgage was at 3.

Customers with a 15-year fixed-rate home loan of $300,000 with today's rates of interest of 2. 26% will pay $1,966. 65 monthly in principal and interest (taxes and charges not included). The Go to this site overall interest paid over the life of the loan will be $53,997. 26. The typical rate on a 5/1 variable-rate mortgage fell 30 basis indicate 2.

16% last week. how does chapter 13 work with mortgages. Last year, the 5/1 ARM was 3. 39%. ARMs are mortgage that have a rates of interest that fluctuates with the marketplace. In the case of 5/1 ARMs, the very first 5 years have a fixed rate and then switch to a variable rate after that. That indicates when the average rate rises or falls, so will your rate.

Home mortgage rates are at record lows, so this could be a suitable time for many folks who wish to conserve cash on their home loan or refinance their current home mortgage. If you're refinancing, know you might pay a slightly greater interest rate because of a brand-new refinancing charge. Debtors who want to get the least expensive rate ought to ensure they have a credit history of at least 760.

Not known Details About What Percentage Of Mortgages Are Fannie Mae And Freddie Mac

In fact, debtors with lower credit rating can be charged one portion point or more higher than customers with excellent or exceptional scores. Prior to you obtain a mortgage, inspect your credit score. Numerous banks and charge card permit you to do this for complimentary. One floating week timeshare definition way you can improve your rating relatively rapidly is to pay for debt.

In addition to your credit history, loan providers will take a look at your debt-to-income ratio, or DTI. This is your overall month-to-month financial obligation divided by your gross month-to-month earnings. It's generally a snapshot of just how much you owe versus just how much you earn. The lower your DTI, the better possibilities you have of getting a lower interest rate.

Finally, research studies have actually revealed that individuals who search tend to get lower rates than those who get a mortgage from the very first loan provider they talk to. Know what the current average rate of interest is in addition to what your credit score, earnings, financial obligation and costs are before you begin applying.

As the Federal Reserve concludes a two-day conference Wednesday, it will be battling with how to react to opposing forces in the nation's COVID-19-fueled recession. On the one hand, a renewal of the infection currently has actually slowed the economy and an even darker winter lays ahead. At the same time, broad availability of a vaccine by spring provides the possibility of a significant improvement.

But Fed officials still have more ammunition, mainly related to their enormous bond-buying stimulus targeted at holding down long-lasting rates that impact home mortgages and other loans. The Fed's policy choice, which will be launched at 2 p. m. on Wednesday, is expected to focus around those bond purchases-- and it could indicate somewhat lower regular monthly costs for homebuyers and other debtors.

The Ultimate Guide To What Is The Current Interest Rate For Mortgages?

Here's the breakdown of what the Fed may do: The Fed is now acquiring $80 billion in Treasury bonds and $40 billion in mortgage-backed securities every month, putting down pressure on long-term rates of interest, such as for mortgages and corporate bonds. The average maturity of the securities it's buying is 7.

Some economic experts expect Fed officials to purchase the same amount of bonds but shift the mix toward those with longer maturities. That would inject more stimulus into the economy by more pushing down rates for mortgages, corporate bonds and other types of loans. COVID-19 is spiking across the nation, with cases, hospitalizations and deaths reaching brand-new records.

Job growth slowed sharply in November and preliminary out of work claims, a rough step of layoffs, jumped greatly to 947,000 the week ending December 5."The economy truly requires," more stimulus, states Oxford economic expert Kathy Bostjancic. "Fed authorities may see the winter infection renewal as the obvious moment to shoot their last bullet," Goldman Sachs said in a research study note. This develops a tidal bore of new work for home loan lenders. Unfortunately, some lending institutions do not have the capability or manpower to process a large number of re-finance loan applications. In this case, a lender might raise its rates to deter new company and offer loan officers time to process loans presently in the pipeline.

Cash-out refinances position a higher risk for home loan lenders, so they're often priced greater than brand-new home purchases and rate-term refinances. Because rates can differ, always go shopping around when buying a home or refinancing a mortgage. Contrast shopping can potentially save thousands, even 10s of countless dollars over the life of your loan.

Some simply go with the bank they utilize for checking and cost savings since that can appear simplest. However, your bank might not offer the best home loan offer for you. And if you're refinancing, your monetary situation may have altered enough that your current loan provider is no longer your best option.

The 25-Second Trick For What Banks Use Experian For Mortgages

When searching for a home mortgage or re-finance, lending institutions will offer a Loan Estimate that breaks down crucial expenses related to the loan. You'll wish to check out these Loan Quotes carefully and compare costs and charges line-by-line, including: Rates of interest Interest rate (APR) Regular monthly mortgage payment Loan origination charges Rate lock costs Closing costs Keep in mind, the most affordable interest rate isn't always the finest deal.

It estimates your total annual cost including interest and fees. Also pay very close attention to your closing costs. Some lending institutions may bring their rates down by charging more in advance by means of discount points. These can add thousands to your out-of-pocket costs. You can also negotiate your home loan rate to get a much better deal (how do adjustable rate mortgages work).

Loan provider An offers the much better rate, but you choose your loan terms from Lending institution B. Speak To Lending institution B and see if they can beat the previous's prices. You might be surprised to discover that a lending institution wants to offer you a lower rate of interest in order to keep your service.

Home loan customers can choose in between a fixed-rate home mortgage and an adjustable-rate home loan (ARM). Fixed-rate home mortgages (FRMs) have interest rates that never change, unless you choose to refinance. This results in foreseeable month-to-month payments and stability over the life of your loan. Adjustable-rate loans have a low interest rate that's repaired for a set variety of years (typically five or 7).

With each rate change, a debtor's mortgage rate can either increase, reduce, or remain the same. These loans are unpredictable given that month-to-month payments can change each year. Adjustable-rate home mortgages are fitting for borrowers who anticipate to move before their first rate adjustment, or who can manage a greater future payment.

Getting The Why Do Mortgage Companies Sell Mortgages To Work

Keep in mind, if rates drop sharply, you are complimentary to refinance and secure a lower rate and payment later. You do not need a high credit history to get approved for a house purchase or refinance, however your credit history will impact your rate. This is since credit rating determines danger level.

For the finest rate, go for a credit rating of 720 or greater. Mortgage programs that don't need a high score consist of: minimum 620 credit rating minimum 500 credit rating (with a 10% down payment) or 580 (with a 3. 5% down payment) no minimum credit score, but 620 is typical minimum 640 credit rating Preferably, you wish to inspect your credit report and score a minimum of 6 months before looking for a home loan.

If you're all set to apply now, it's still worth checking so you have an excellent idea of what loan programs you may qualify for and how your score will affect your rate. You can get your credit report from AnnualCreditReport. com and your rating from MyFico. com. Nowadays, home loan programs don't require the traditional 20 percent down.

Down payment minimums differ depending upon the loan program. For instance: need a deposit between 3% and 5% require 3. 5% down allow absolutely no deposit normally require a minimum of 5% to 10% down Remember, a higher deposit lowers your risk as a borrower and helps you negotiate a better home loan rate.

This is an included expense paid by the customer, which safeguards their lender in case of default or foreclosure. However a big deposit is not needed. For many individuals, it makes good sense to make a smaller deposit in order to purchase a house earlier and begin building house equity.

The Facts About What Are Interest Rates Now For Mortgages Revealed

The five primary kinds of home loans include: Your interest rate remains the very same over the life of the loan. This is a good choice for borrowers who anticipate to live in their homes long-term. The most popular loan choice is the 30-year home mortgage, however 15- and 20-year terms are also commonly readily available.

Then, your home loan rate resets every year. Your rate and payment can rise or fall annually depending upon how the wider interest rate trends. ARMs are perfect for customers who expect to move prior to their very first rate modification (typically in 5 or 7 years). For those who prepare to remain in their home long-lasting, a fixed-rate home loan is usually recommended.

In 2020, the conforming loan limit is $510,400 in many areas. Jumbo loans are perfect for borrowers who need a bigger loan to purchase a high-priced property, specifically in huge cities with high realty worths. A federal government loan backed by the Federal Housing Administration for low- to moderate-income borrowers.

A government loan backed by the Department of Veterans Affairs. To be eligible, you should be active-duty military, a veteran, a Reservist or National Guard service member, or an eligible spouse. VA loans allow no deposit and have incredibly low home loan rates. USDA loans are a government program backed by the U.S.

They use a no-down-payment solution for customers who buy genuine estate in a qualified rural location. To qualify, your earnings needs to be at or listed below the regional average. Debtors can receive a home mortgage without tax returns, utilizing their personal or company bank account. This is a choice for self-employed or seasonally-employed debtors.

A Biased View of What Is The Current Index Rate For Mortgages

This provides lenders the flexibility to set their own guidelines. Non-QM loans might have lower credit report requirements, or offer low-down-payment options without home loan insurance. The lender or loan program that's right for someone might not be right for another. Explore your choices and then pick a loan based upon your credit history, deposit, and financial goals, as well as regional home prices.

Normally, it just takes a few hours to get quotes from multiple lending institutions and it could save you thousands in the long run. We receive existing home loan rates each day from a network of home loan loan providers that provide house purchase and refinance loans. Mortgage rates shown here are based on sample customer profiles that vary by loan type.